UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K/A

Amendment No. 1

(Mark One)

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the Fiscal Year Ended December 31, 2017

or

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934

Commission File No. 1-32630

Fidelity National Financial, Inc.

(Exact name of registrant as specified in its charter)

|

Delaware |

|

16-1725106 |

|

(State or other jurisdiction of |

|

(I.R.S. Employer |

|

601 Riverside Avenue |

|

|

|

Jacksonville, Florida 32204 |

|

(904) 854-8100 |

|

(Address of principal executive offices, including zip code) |

|

(Registrant’s telephone number, |

|

|

|

including area code) |

Securities registered pursuant to Section 12(b) of the Act:

|

Title of Each Class |

|

Name of Each Exchange on Which Registered |

|

FNF Group Common Stock, $0.0001 par value |

|

New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K, or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated filer |

|

x |

|

Accelerated filer |

|

o |

|

|

|

|

|

|

|

|

|

Non-accelerated filer |

|

o (Do not check if a smaller reporting company) |

|

Smaller reporting company

|

|

o |

|

|

|

|

|

Emerging growth company |

|

o |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

The aggregate market value of the shares of FNF common stock held by non-affiliates of the registrant as of June 30, 2017 was $8,461,286,198 based on the closing price of $32.37 as reported by the New York Stock Exchange.

As of April 16, 2018, there were 274,588,956 shares of FNF common stock outstanding.

EXPLANATORY NOTE

This Amendment No. 1 (the “Amendment”) on Form 10-K/A is being filed with respect to the Registrant’s Annual Report on Form 10-K for the fiscal year ended December 31, 2017 filed with the Securities and Exchange Commission on February 23, 2018 (the “Form 10-K”). This Amendment updates Part III in its entirety to contain the information required therein.

Except for the changes to Part III and the filing of related certifications added to the list of Exhibits in Part IV, this Amendment makes no changes to the Form 10-K. This Amendment does not reflect events occurring after the filing of the Form 10-K or modify disclosures affected by subsequent events.

FIDELITY NATIONAL FINANCIAL, INC.

FORM 10-K/A

|

|

|

Page |

|

|

|

|

|

|

| |

|

|

|

|

|

1 | ||

|

|

|

|

|

7 | ||

|

|

|

|

|

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS |

42 | |

|

|

|

|

|

CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE |

44 | |

|

|

|

|

|

53 | ||

|

|

|

|

|

|

| |

|

|

|

|

|

54 |

Item 10. DIRECTORS AND OFFICERS OF THE REGISTRANT

Certain Information about our Directors

Certain biographical information for our directors is below.

Class I Directors—Term Expiring 2018

|

Name |

|

Position with FNF |

|

Age |

|

Raymond R. Quirk |

|

Chief Executive Officer and Director |

|

71 |

|

Heather H. Murren |

|

Member of the Audit Committee |

|

51 |

|

John D. Rood |

|

Member of the Audit Committee |

|

63 |

Raymond R. Quirk. Raymond R. Quirk has served as Chief Executive Officer of Fidelity National Financial, Inc. (FNF or the Company) since December 2013 and as a director of FNF since February 2017. Previously, he served as the President of FNF and he has served in that position since April 2008. Previously, Mr. Quirk served as Co-President since May 2007 and Co-Chief Operating Officer of FNF from October 2006 until May 2007. Mr. Quirk was appointed as President of FNF in 2002. Since joining FNF in 1985, Mr. Quirk has served in numerous executive and management positions, including Executive Vice President, Co-Chief Operating Officer and Division Manager and Regional Manager, with responsibilities for managing direct and agency operations nationally. Mr. Quirk also serves on the board of directors of J. Alexander’s Holdings, Inc.

Mr. Quirk’s qualifications to serve on the FNF board of directors include his more than 30 years of experience with FNF, his deep knowledge of our business and industry and his strong leadership abilities.

Heather H. Murren. Ms. Murren is a private investor. She retired as a Managing Director and group head of Global Securities and Economics at Merrill Lynch in 2002 after more than a decade on Wall Street. In 2002, Ms. Murren founded the nonprofit Nevada Cancer Institute, a cancer research and treatment center, where she served as Chairman and CEO and then as a board member until the institute merged into Roseman University in 2013. She was appointed by Congress to serve on the Financial Crisis Inquiry Commission from 2009 to 2011. The Commission’s findings, “The Financial Crisis Inquiry Report” was listed on the New York Times bestseller list. Ms. Murren was appointed and served as a Commissioner on the White House Commission on Enhancing National Cybersecurity in 2016. The Commissions’ findings were presented to President Obama in December 2016. She serves on the Board of Trustees of the Johns Hopkins University and the Johns Hopkins University Applied Physics Laboratory and formerly served on the board of Mannkind Corporation.

Ms. Murren’s qualifications include her strong background in finance gained during her time at Merrill Lynch, her leadership experience as a group leader at a leading Wall Street firm and as founder, Chair and CEO at various non-profits, and her regulatory and cyber-security knowledge from serving on the Financial Crisis Inquiry Commission and Commission on Enhancing National Cybersecurity.

John D. Rood. Mr. Rood has served on our board of directors since May 2013. Mr. Rood is the founder and Chairman of The Vestcor Companies, a real estate firm with more than 30 years of experience in multifamily development and investment. Mr. Rood also serves on the board of directors of Black Knight, Inc. (Black Knight). From 2004 to 2007, Mr. Rood served as the US Ambassador to the Commonwealth of the Bahamas. Mr. Rood previously served on the board of Alico, Inc., and currently serves on several private boards. He was appointed by Governor Jeb Bush to serve on the Florida Fish and Wildlife Commission where he served until 2004. He was appointed by Governor Charlie Crist to the Florida Board of Governors, which oversees the State of Florida University System, where he served until 2013. Mr. Rood was appointed by Mayor Lenny Curry to the JAXPORT Board of Directors, where he served from October 2015 to July 2016. Governor Rick Scott appointed Mr. Rood to the Florida Prepaid College Board in July 2016, where Mr. Rood serves as Chairman of the Board, and to the Enterprise Florida, Inc. board of directors in September 2016. Mr. Rood has participated in numerous risk and audit training programs with KPMG, Booz Allen and the National Association of Corporate Directors. He is a Board Leadership Fellow with NACD.

Mr. Rood’s qualifications to serve on the FNF board of directors include his experience in the real estate industry, his leadership experience as a United States Ambassador, his financial literacy and his experience as a director on boards of both public and private companies.

Class II Directors—Term Expiring 2019

|

Name |

|

Position with FNF |

|

Age |

|

Richard N. Massey |

|

Lead Director |

|

62 |

|

|

|

Chairman of the Compensation Committee |

|

|

|

|

|

Member of the Corporate Governance and Nominating Committee and the Executive Committee |

|

|

|

Janet Kerr |

|

Director |

|

63 |

|

Daniel D. (Ron) Lane |

|

Member of the Compensation Committee |

|

83 |

|

Cary H. Thompson |

|

Member of the Compensation Committee and the Executive Committee |

|

61 |

Richard N. Massey. Mr. Massey has served as a director of the Company since 2006. Mr. Massey has been a partner of Westrock Capital, LLC, a private investment partnership, since January 2009. Mr. Massey was Chief Strategy Officer and General Counsel of Alltel Corporation from January 2006 to January 2009. From 2000 until 2006, Mr. Massey served as Managing Director of Stephens Inc., a private investment bank, during which time his financial advisory practice focused on software and information technology companies. Mr. Massey also serves as a director of Black Knight and FGL Holdings, and as a director of Oxford American Literary Project and as Chairman of the Arkansas Razorback Foundation. Mr. Massey formerly served as a director of Fidelity National Information Services, Inc. (FIS) and Bear State Financial, Inc.

Mr. Massey’s qualifications to serve on the FNF board include his experience in corporate finance and investment banking and as a financial and legal advisor to public and private businesses, as well as his expertise in identifying, negotiating and consummating mergers and acquisitions.

Janet Kerr. Ms. Kerr has served as a director FNF since March 2016. Ms. Kerr is Vice-Chancellor of Pepperdine University and Professor Emeritus of Law at Pepperdine University School of Law where she taught for 30 years and was awarded the Laure Sudreau-Rippe Endowed Chair in 2011. She is also currently Of Counsel to Nave & Cortell. Having developed several successful technology companies, Ms. Kerr provides expertise in startup counseling; corporate organization and governance; mergers, acquisitions, and other strategic relationships; and seed, angel, venture capital and other financing arrangements. Ms. Kerr also serves as Chief Executive Officer of Kerr Strategic Consulting. Ms. Kerr has extensive board experience. She currently serves on the boards of La-Z-Boy, Inc., Tilly’s, Inc., and AppFolio Inc., and currently or has in the past served as chair of the corporate governance and nominating committees of each of these companies. Ms. Kerr formerly served on the boards of TCW Strategic Income Fund, Inc., TCW Funds and CKE Restaurants, Inc. She has also served as a consultant to various companies regarding Sarbanes-Oxley Act compliance and corporate governance. Ms. Kerr is a well-known author in the areas of securities, corporate law and corporate governance, having published numerous articles and a book on the subjects. Ms. Kerr was appointed by ISS/Risk Metrics to serve on the Governance Exchange Advisory Council, and she served as a Director/Member of Advisory Board at Larta Institute. She is also a member of the National Association of Corporate Directors and Women Corporate Directors.

Ms. Kerr’s qualifications to serve on the FNF board of directors include her more than 30 years of corporate governance experience, which uniquely positions Ms. Kerr to contribute to our board, and her significant expertise in the regulatory, governance and legal matters of public companies.

Daniel D. (Ron) Lane. Mr. Lane has served as a director of the Company since 2005, and as a director of predecessors of FNF since 1989. Since February 1983, Mr. Lane has been a principal, Chairman and Chief Executive Officer of Lane/Kuhn Pacific, Inc., a corporation comprising several community development and home building partnerships, all of which are headquartered in Newport Beach, California. Mr. Lane served as a director of CKE Restaurants, Inc. from 1993 through 2010, and served as a director of FIS from February 2006 to July 2008, and as a director of LPS from July 2008 until March 2009. Mr. Lane is also a member of the Board of Trustees of the Univeristy of Southern California.

Mr. Lane’s qualifications to serve on the FNF board include his extensive experience in and knowledge of the real estate industry, particularly as Chairman and Chief Executive Officer of Lane/Kuhn Pacific, Inc., his financial literacy and his experience as a member of the boards of directors of other companies.

Cary H. Thompson. Cary H. Thompson has served as a director of the Company since 2005, and as a director of predecessors of FNF since 1992. Mr. Thompson currently is Executive Vice Chairman of Global Corporate and Investment Banking, Bank of America Merrill Lynch, having joined that firm in May 2008. From 1999 to May 2008, Mr. Thompson was Senior Managing Director and Head of West Coast Investment Banking at Bear Stearns & Co., Inc. Mr. Thompson served as a director of FIS from February 2006 to July 2008, as a director of Lender Processing Services, Inc. (LPS) from July 2008 to March 2009, and on the board of managers of Black Knight Financial Services, LLC (BKFS LLC) from January 2014 until April 2015.

Mr. Thompson’s qualifications to serve on the FNF board include his experience in corporate finance and investment banking, his knowledge of financial markets and his expertise in negotiating and consummating financial transactions.

Class III Directors—Term Expiring 2020

|

Name |

|

Position with FNF |

|

Age |

|

William P. Foley, II |

|

Non-executive Chairman of the Board |

|

73 |

|

Douglas K. Ammerman |

|

Chairman of the Audit Committee |

|

66 |

|

Thomas M. Hagerty |

|

Director |

|

55 |

|

Peter O. Shea, Jr. |

|

Chairman of the Corporate Governance and Nominating Committee |

|

51 |

William P. Foley, II. Mr. Foley has served as Chairman of the board of directors of FNF since 2005, and as a director of predecessors of FNF since 1984. Mr. Foley served as Executive Chairman of FNF from October 2006 until January 2016. Mr. Foley served as Chief Executive Officer of FNF from 1984 until May 2007 and as President of FNF from 1984 until December 1994. Mr. Foley has also served as Executive Chairman of Black Knight and its predecessors since January 2014, as Co-Executive Chairman of FGL Holdings since April 2016, and as Executive Chairman of Cannae Holdings, Inc. (Cannae) since November 2017. Mr. Foley served as Vice Chairman of the board of directors of FIS from March 2012 through May 2017. Prior to that, he served as Executive Chairman of FIS from February 2006 through February 2011 and as non-executive Chairman of FIS from February 2011 to March 2012. Within the past five years, Mr. Foley formerly served as a director of Remy International, Inc. Mr. Foley also serves on the boards of directors of The Foley Family Charitable Foundation, Inc. and the Cummer Museum of Arts and Gardens, and is a founder, trustee and director of The Folded Flag Foundation, Inc. Mr. Foley also is Chairman, CEO and President of Foley Family Wines Holdings, Inc., which is the holding company of numerous vineyards and wineries located in the U.S. and in New Zealand, and Executive Chairman and Chief Executive Officer of Black Knight Sports and Entertainment LLC, which is the company that owns the Vegas Golden Knights, a National Hockey League team. After receiving his B.S. degree in engineering from the United States Military Academy at West Point, Mr. Foley served in the U.S. Air Force, where he attained the rank of captain.

Mr. Foley’s qualifications to serve on the FNF board of directors include his more than 30 years as a director and executive officer of FNF, his experience as a board member and executive officer of public and private companies in a wide variety of industries, and his strong track record of building and maintaining shareholder value and successfully negotiating and implementing mergers and acquisitions.

Douglas K. Ammerman. Mr. Ammerman has served as a director of the Company since 2005. Mr. Ammerman is a retired partner of KPMG LLP, where he became a partner in 1984. Mr. Ammerman formally retired from KPMG in

2002. He also serves as a director of William Lyon Homes, Stantec Inc. and J. Alexander’s Holdings Inc. Mr. Ammerman formerly served on the boards of Remy International, Inc. and El Pollo Loco, Inc.

Mr. Ammerman’s qualifications to serve on the FNF board of directors include his financial and accounting background and expertise, including his 18 years as a partner with KPMG, and his experience as a director on the boards of other companies.

Thomas M. Hagerty. Mr. Hagerty has served as a director of the Company since 2005, and as a director of predecessors of FNF since 2005. Mr. Hagerty is a Managing Director of Thomas H. Lee Partners, L.P. Mr. Hagerty has been employed by Thomas H. Lee Partners, L.P. and its predecessor, Thomas H. Lee Company, since 1988. Mr. Hagerty currently serves as a director of Black Knight, FleetCor Technologies, Ceridian HCM Holdings, Inc., FIS and several private companies. Mr. Hagerty formerly served as a director of First Bancorp and MoneyGram International, Inc.

Mr. Hagerty’s qualifications to serve on the FNF board of directors include his managerial and strategic expertise working with large growth-oriented companies as a Managing Director of Thomas H. Lee Partners, L.P., a leading private equity firm, and his experience in enhancing value at such companies, along with his expertise in corporate finance.

Peter O. Shea, Jr. Peter O. Shea, Jr. has served as a director of the Company since April 2006. Mr. Shea is the President and Chief Executive Officer of J.F. Shea Co., Inc., a private company with operations in home building, commercial property development and management and heavy civil construction. Prior to his service as President and Chief Executive Officer, he served as Chief Operating Officer of J.F. Shea Co., Inc.

Mr. Shea’s qualifications to serve on the FNF board of directors include his experience in managing multiple and diverse operating companies and his knowledge of the real estate industry, particularly as President and Chief Executive Officer of J.F. Shea Co., Inc.

Certain Information About our Executive Officers

The executive officers of the Company are set forth in the table below, together with biographical information, except for Mr. Quirk, whose biographical information is included in this Annual Report on Form 10-K under the section titled “Certain Information about our Directors — Information About the Director Nominees and Continuing Directors.”

|

Name |

|

Position with FNF |

|

Age |

|

Raymond R. Quirk |

|

Chief Executive Officer |

|

71 |

|

Michael J. Nolan |

|

President |

|

58 |

|

Roger Jewkes |

|

Chief Operating Officer |

|

59 |

|

Brent B. Bickett |

|

Executive Vice President—Corporate Strategy |

|

53 |

|

Anthony J. Park |

|

Executive Vice President and Chief Financial Officer |

|

51 |

|

Peter T. Sadowski |

|

Executive Vice President and Chief Legal Officer |

|

63 |

|

Michael L. Gravelle |

|

Executive Vice President, General Counsel and Corporate Secretary |

|

56 |

Michael J. Nolan. Mr. Nolan has served as President of the Company since January 2016. He served as the Co-Chief Operating Officer from September 2015 until January 2016. Additionally, he has served as President of Eastern Operations for Fidelity National Title Group since January 2013 and Executive Vice President-Division Manager since May 2010. Previously, Mr. Nolan served as Regional Manager from 2003 through 2010 and state and branch manager positions from 1998-2003. Since joining company in 1983, Mr. Nolan has served in numerous executive and management positions, including President, Executive Vice President, Division Manager and Regional Manager, with responsibilities for managing direct and agency operations for the Midwest and East coast. Also, Mr. Nolan has overall responsibility for the Company’s operations in Canada as well as IPX, Fidelity’s 1031 exchange company, and FRS, Fidelity’s relocation company.

Roger Jewkes. Mr. Jewkes has served as Chief Operating Officer of FNF since January 2016, and served as Co-Chief Operating Officer from September 2015 to January 2016. Previously, he served as an Executive Vice President of FNF and was appointed to that position in 2001. Since joining FNF through an acquisition in 1987, Mr. Jewkes has served in several executive and operational management positions including President of Western Operations, Executive Vice President, Division Manager and Regional Manager, with responsibilities for managing a significant number of direct operations along with some ancillary companies held by FNF.

Brent B. Bickett. Mr. Bickett has served as Executive Vice President of Corporate Strategy of FNF since January 2016. Mr. Bickett served as President of FNF from December 2013 until January 2016. Mr. Bickett has primary responsibility for managing FNF’s merger and acquisition activities, strategic initiatives, portfolio investments and investor relations group. Mr. Bickett joined FNF in 1999 and served as Executive Vice President, Corporate Finance, of FNF from 2003 to 2013. Mr. Bickett has also served as President of Cannae since July 2017.

Anthony J. Park. Mr. Park has served as Executive Vice President and Chief Financial Officer of FNF since October 2005. Prior to being appointed CFO of the Company, Mr. Park served as Controller and Assistant Controller of FNF from 1991 to 2000 and served as the Chief Accounting Officer of FNF from 2000 to 2005.

Peter T. Sadowski. Mr. Sadowski has served as Executive Vice President and Chief Legal Officer of FNF since 2008. Prior to that, Mr. Sadowski served as Executive Vice President and General Counsel of FNF since 1999. Mr. Sadowski has also served as Executive Vice President and Chief Legal Officer of Cannae since July 2017. Mr. Sadowski also is a member of the California Coastal Conservancy.

Michael L. Gravelle. Mr. Gravelle has served as the Executive Vice President, General Counsel and Corporate Secretary of FNF since January 2010 and served in the capacity of Executive Vice President, Legal since May 2006 and Corporate Secretary since April 2008. Mr. Gravelle joined FNF in 2003, serving as Senior Vice President. Mr. Gravelle joined a subsidiary of FNF in 1993, where he served as Vice President, General Counsel and Secretary beginning in 1996 and as Senior Vice President, General Counsel and Corporate Secretary beginning in 2000. Mr. Gravelle has also served as Executive Vice President, General Counsel & Corporate Secretary of Black Knight, Inc. and its predecessors since January 2014, and as Executive Vice President, General Counsel and Corporate Secretary of Cannae Holdings, Inc., since July 2017. He served as Senior Vice President, General Counsel and Corporation Secretary of Remy from February 2013 until March 2015.

Section 16(a) Beneficial Ownership Reporting Compliance

Section 16 of the Securities Exchange Act of 1934, requires the Company’s executive officers and directors to file reports of their ownership, and changes in ownership, of the Company’s common stock with the Securities and Exchange Commission. Executive officers and directors are required by the Securities and Exchange Commission’s regulations to furnish the Company with copies of all forms they file pursuant to Section 16 and the Company is required to report in this Annual Report on Form 10-K any failure of its directors and executive officers to file by the relevant due date any of these reports during fiscal year 2017. Based solely upon a review of these reports, we believe all directors and executive officers of the Company complied with the requirements of Section 16(a) in 2017.

Code of Ethics and Business Conduct

Our board of directors has adopted a Code of Ethics for Senior Financial Officers, which is applicable to our Chief Executive Officer, our Chief Financial Officer and our Chief Accounting Officer, and a Code of Business Conduct and Ethics, which is applicable to all our directors, officers and employees. The purpose of these codes is to: (i) promote honest and ethical conduct, including the ethical handling of conflicts of interest; (ii) promote full, fair, accurate, timely and understandable disclosure; (iii) promote compliance with applicable laws and governmental rules and regulations; (iv) ensure the protection of our legitimate business interests, including corporate opportunities, assets and confidential information; and (v) deter wrongdoing. Our codes of ethics were adopted to reinvigorate and renew our commitment to our longstanding standards for ethical business practices. Our reputation for integrity is one of our most important assets and each of our employees and directors is expected to contribute to the care and preservation of that asset. Under our codes of ethics, an amendment to or a waiver or modification of any ethics policy applicable to our directors or executive officers must be disclosed to the extent required under Securities and Exchange

Commission and/or New York Stock Exchange rules. We intend to disclose any such amendment or waiver by posting it on the Investor Relations page of our website at www.fnf.com.

Copies of our Code of Business Conduct and Ethics and our Code of Ethics for Senior Financial Officers are available for review on the Investor Relations page of our website at www.fnf.com. Shareholders may also obtain a copy of any of these codes by writing to the Corporate Secretary at the address set forth under “Available Information” below.

Audit Committee

The members of the audit committee are Douglas K. Ammerman (Chair), Heather H. Murren and John D. Rood. The board has determined that each of the audit committee members is financially literate and independent as required by the rules of the Securities and Exchange Commission and the New York Stock Exchange, and that each of Mr. Ammerman, Ms. Murren and Mr. Rood is an audit committee financial expert, as defined by the rules of the Securities and Exchange Commission. The board of directors also reviewed Mr. Ammerman’s service on the audit committee in light of his concurrent service on the audit committees of four other companies. The board of directors considered Mr. Ammerman’s extensive financial and accounting background and expertise as a former partner of KPMG, his knowledge of our company and understanding of our financial statements as a long-time director and audit committee member, and the fact that Mr. Ammerman is retired from active employment, and determined that Mr. Ammerman’s service on the audit committees of four public companies, including FNF’s audit committee, would not impair his ability to effectively serve on FNF’s audit committee. The audit committee met nine times in 2017.

The primary functions of the audit committee include:

· appointing, compensating and overseeing our independent registered public accounting firm;

· overseeing the integrity of our financial statements and our compliance with legal and regulatory requirements;

· discussing the annual audited financial statements and unaudited quarterly financial statements with management and the independent registered public accounting firm;

· establishing procedures for the receipt, retention and treatment of complaints (including anonymous complaints) we receive concerning accounting, internal accounting controls, auditing matters or potential violations of law;

· approving audit and non-audit services provided by our independent registered public accounting firm;

· discussing earnings press releases and financial information provided to analysts and rating agencies;

· discussing with management our policies and practices with respect to risk assessment and risk management;

· reviewing any material transaction between our chief financial officer or chief accounting officer that has been approved in accordance with our Code of Ethics for Senior Financial Officers, and providing prior written approval of any material transaction between us and our chief executive officer; and

· producing an annual report for inclusion in our proxy statement, in accordance with applicable rules and regulations.

The audit committee is a separately-designated standing committee established in accordance with Section 3(a)(58)(A) of the Securities Exchange Act of 1934, as amended.

Item 11. EXECUTIVE COMPENSATION

COMPENSATION DISCUSSION AND ANALYSIS AND EXECUTIVE AND

DIRECTOR COMPENSATION

Compensation Discussion and Analysis

The following discussion and analysis of compensation programs should be read with the compensation tables and related disclosures that follow. This discussion contains forward-looking statements that are based on our current plans and expectations regarding future compensation programs. Compensation programs that we adopt in the future may differ materially from the programs summarized in this discussion. The following discussion may also contain statements regarding corporate performance targets and goals. These targets and goals are disclosed in the limited context of our compensation programs and should not be understood to be statements of management’s expectations or estimates of results or other guidance. We specifically caution investors not to apply these statements to other contexts.

In this compensation discussion and analysis, we provide an overview of our approach to compensating our named executive officers in 2017, including the objectives of our compensation programs and the principles upon which our compensation programs and decisions are based. Our named executive officers, and their titles, in 2017 were:

· Raymond R. Quirk, our Chief Executive Officer;

· Michael J. Nolan, our President;

· Brent B. Bickett, our Executive Vice President, Corporate Strategy;

· Roger S. Jewkes, our Chief Operating Officer; and

· Anthony J. Park, our Executive Vice President and Chief Financial Officer.

EXECUTIVE SUMMARY

The Split-Off of FNFV Group and Spin-Off Black Knight

On September 29, 2017 we completed our tax-free distribution to our FNF Group shareholders of all 83.3 million shares of New BKH Corp., or New BKH, common stock that we previously owned, which we refer to as the Spin-Off. Immediately following the Spin-Off, New BKH and our majority-owned subsidiary Black Knight Financial Services, Inc., or BKFS, engaged in a series of transactions resulting in the formation of a new publicly-traded holding company, Black Knight, Inc., or Black Knight, which owns all of the outstanding shares of BKFS. In the Spin-Off, holders of FNF Group common stock received approximately 0.30663 shares of Black Knight common stock for each share of FNF Group common stock held at the close of business on September 20, 2017. Black Knight’s common stock is listed under the symbol “BKI” on the New York Stock Exchange. The Spin-Off is expected to generally be tax-free to FNF Group shareholders for U.S. federal income tax purposes, except to the extent of any cash received in lieu of Black Knight’s fractional shares.

On November 17, 2017 we completed our previously announced split-off, which we refer to as the Split-Off, of our former wholly-owned subsidiary Cannae Holdings, Inc., or Cannae, which consists of the businesses, assets and liabilities formerly attributed to our Fidelity National Financial Ventures Group, or FNFV Group, including Ceridian Holding, LLC, American Blue Ribbon Holdings, LLC and T-System Holding LLC. The Split-Off was accomplished by our redemption of all of the outstanding shares of our FNFV Group common stock for outstanding shares of common stock of Cannae on a one-for-one basis.

Both Cannae and Black Knight are independent publicly-traded companies, and FNFV group shares are no longer outstanding. These transactions positively impacted our executive compensation programs by allowing us to continue simplifying these programs and renew focus on our core title operations.

Financial Highlights

FNF has performed well for our shareholders over the past several years. In 2017, we generated approximately $7.7 billion in total revenue (a 5.6% increase from 2016), and approximately $771 million in net earnings (an 18.6% increase from 2016). As reflected in the charts below, from 2015 through 2017, we have delivered strong growth in total revenue and net earnings.

During this three year period, from January 1, 2015 through December 31, 2017, we delivered a total return to our shareholders of 60.1%, compared to S&P 500 total return of 36.6% during the same period. This includes a return of approximately $278 million to our shareholders in the form of cash dividends. Total shareholder return is based on stock price changes as adjusted to account for the Black Knight Spin-Off in 2017 (assuming that the underlying shares were sold on the spin-off closing date) and cash dividends paid.

Pay for Performance

The primary goal of our executive compensation programs in 2017 was to drive continued growth and successful execution of our strategic business objectives. We believe our programs achieve this goal by:

· tying material portions of our named executive officers’ compensation to the performance of our core title operations;

· structuring our performance-based programs to focus our named executive officers on attaining pre-established, objectively-determinable key performance goals that are aligned with and support our key strategic business objectives in our various operations, which, in turn, are aimed at growing long-term shareholder value for our shareholders;

· recognizing our executives’ leadership abilities, scope of responsibilities, experience, effectiveness, and individual performance achievements; and

· attracting, motivating, and retaining a highly qualified and effective management team that can deliver superior performance and build shareholder value over the long term.

As in past years, there was a direct correlation between our named executive officers’ pay and our performance in 2017. Here are a few highlights:

· We far exceeded both our adjusted title revenue and adjusted title pre-tax profit margin goals as set by our compensation committee under our annual incentive plan. Consistent with this strong performance, our named executive officers earned an annual incentive equal to 200% of their respective target annual incentive opportunities. See the “FNF Annual Incentive Performance Measures and Results” section below.

· We far exceeded the quarterly adjusted title pre-tax profit margin goals set by our compensation committee as performance criteria for our 2016 restricted stock awards. As a result, we expect these awards to fully vest, subject to each executive’s continued employment with us to satisfy the time-based vesting requirements for those awards.

· Prior to the Split-Off, our FNFV Group created substantial value for our FNFV Group shareholders with our investment in One Digital, which we sold on June 6, 2017 for $560 million, representing a 4.6x cash on cash return multiple and a 41% IRR. After repayment of debt, payout to option holders and a minority equity investor and other transaction related payments, FNFV Group received $331 million from the sale, which includes $326 million of cash and $5 million of purchase price holdback receivable.

Note that the financial measures used as performance targets for our named executive officers described in this discussion are non-GAAP measures and differ from the comparable GAAP measures reported in our financial statements. The measures are adjusted to exclude the impact of certain non-recurring and other items. We explain how we calculate these measures in the “Analysis of Compensation Components” section below.

Shareholder Vote on 2016 Executive Compensation

At our 2017 annual meeting of shareholders, we held a non-binding advisory vote, also called a “say on pay” vote, on the compensation of our named executive officers as disclosed in the 2017 proxy statement. A majority of our shareholders approved our “say on pay” proposal, with approximately 70% of the votes cast in favor of the proposal and approximately 30% of the votes cast against the proposal. This reflects significantly more support than at our 2016 annual meeting of shareholder where only 54% of our shareholders approved our “say on pay” proposal. The compensation committee considered these results when evaluating our executive compensation program.

Shareholder Outreach and Changes to our Compensation Programs in 2017

Our compensation committee is committed to listening and responding to the views of our shareholders in creating and tailoring our executive compensation programs. Following the 2017 annual meeting of shareholders and the 2016 “say on pay” shareholder vote, our President, Chief Financial Officer, and Treasurer met with our investors in break-out sessions at investor conferences, as well as in independent one-on-one investor meetings, to discuss our business and stock price performance, as well as discuss and receive feedback on our compensation programs. In this regard, we met with investors at more than 13 investor conferences and numerous one-on-one meetings. The investors with whom we met in 2017 represented 13 of our top 20 shareholders, who collectively owned more than 40% of our shares as of December 31, 2017.

We believe that we have been highly responsive to our shareholders’ concerns, and have created and continued compensation programs that achieved our strategic corporate objectives, focused our executives on achieving superior operating results and shareholder returns, balanced short-term and long-term incentives, and maintained a strong correlation between pay and performance.

Improvements to our Compensation Programs

In response to feedback received during our investor outreach efforts, and the analysis of our compensation programs by proxy advisory firms, we have made a number of improvements to our compensation programs over the last four years to address concerns raised by our shareholders and proxy advisory firms. Following are highlights of the key changes, demonstrating the responsiveness of our compensation committee:

|

Areas of Improvement |

|

Improvements |

|

Pay Programs Have Been Simplified |

|

We continued to simplify our compensation programs. In 2017, our named executive officers earned base salary, an annual performance-based cash incentive, restricted stock awards and standard employee benefits. Messrs. Bickett and Park also received a payment under our legacy Investment Success Incentive Plan. Further simplifying our incentive program, the Investment Success Incentive Plan was assumed by Cannae in connection with the Split-Off and will no longer be a |

|

|

|

component of our incentive program. Finally, in 2017, our named executive officers’ long-term equity awards continued to consist only of restricted stock awards, all of which had performance- and time-based vesting conditions. No named executive officer received only time-based equity awards in 2017 and no named executive officer received an equity award granted outside our formulaic long-term incentive program (a “one-off” award) in 2017. |

|

|

|

|

|

The Split-Off and Black Knight Spin-Off |

|

In anticipation of the Split-Off we did not issue any FNFV equity incentive awards in 2017. Further, as discussed below, our Investment Success Incentive Plan was assumed by Cannae in connection with the Split-Off. The assumption of the Investment Success Incentive Plan will simplify our compensation programs. For purposes of the CD&A, we will no longer need to distinguish between our core and non-core businesses and we will no longer need to discuss tracking stocks, awards earned under the Investment Success Incentive Plan following the Split-Off, and Black Knight compensation earned following the Black Knight Spin-Off. |

|

|

|

|

|

Annual Incentive Plan Performance Goals are Rigorously Set, Despite Volatile and Unpredictable Economic Environment |

|

The adjusted title revenue and adjusted pre-tax title margin performance targets under our 2017 annual incentive plan were approximately 3% higher and 0.5% lower than the targets under our 2016 plan, respectively. Our annual incentive plan targets correlate with our annual strategic financial plans, which are based on our forecasted originations for the year and the relative mix of purchase versus refinance originations. Further, these annual incentive plan targets have a significant impact on long-term stock price. These expectations are based on forecasts provided by the Mortgage Bankers Association (MBA), Fannie Mae, anticipated changes in interest rates and recent and expected industry and company trends. We prepare a base plan as well as upside and downside scenarios, which, taken together, form the strategic financial plan and the basis of the performance targets. When we set our 2017 performance targets in March 2017, our assumptions included a decline in refinance volumes of 49%, a 2% increase in the residential purchase market, and a 6% decline in the national commercial market. In light of these assumptions, the adjusted title revenue and adjusted pre-tax title margin performance targets were rigorous. Our 2017 results exceeded these performance targets due to numerous factors, including a 4% increase in agency title insurance premiums driven by our active management of our agent portfolio, a 3% increase in direct title insurance premiums, and enhancements to our underwriting processes which have resulted in lower |

|

|

|

policy year loss ratios. Our executives’ performance directly affected each of these factors. |

|

|

|

|

|

Long-Term Performance Goals are Rigorously Set, Despite Volatile and Unpredictable Economic Environment |

|

The pre-tax title margin performance target applicable to our restricted stock awards granted in 2017 was approximately 0.5% higher than the target under our 2016 awards. This target is based on the forecasts discussed above. Our executives’ strong performance in 2017 led to our far exceeding these goals. |

Governance and Compensation Best Practices

We periodically review our compensation programs and make adjustments that are believed to be in the best interests of our company and our shareholders. As part of this process, we review compensation trends and consider current best practices, and make changes in our compensation programs when we deem it appropriate, all with the goal of continually improving our approach to executive compensation.

Some of the best practices adopted by our compensation committee or full board of directors include the following:

|

Things We Do: |

|

Things We Don’t Do: |

|

x Permit shareholder action by written consent x Separate the positions of Chief Executive Officer and Chairman of the Board x An independent lead director to help manage the affairs of our Board x Deliver total compensation predominantly through variable pay x Allow “proxy access” x Have majority voting in uncontested director elections x Maintain robust stock ownership requirements x Maintain a clawback policy for incentive based compensation x Have a high ratio of performance-based compensation to total compensation, and a low ratio for fixed benefits/perquisites (non-performance-based compensation) x Undertake an annual review of compensation risk x Limit perquisites x Have performance-based vesting provision in restricted stock grants to our officers, including our named executive officers x Require that any dividends or dividend equivalents on restricted stock and other |

|

x Have supermajority voting provisions in our Certificate of Incorporation x Provide tax gross-ups or reimbursement of taxes on perquisites x Have liberal change in control definitions x Include modified single-trigger severance provisions — which provide severance upon a voluntary termination of employment following a change in control — in our executive agreements x Allow hedging and pledging transactions involving our securities x Have multi-year guarantees for salary increases, non-performance based bonuses or guaranteed equity compensation in our executive employment agreements

|

|

awards that are subject to performance based vesting conditions are subject to the same underlying vesting requirements applicable to the awards—that is, no payment of dividends or dividend equivalents are made unless and until the award vests; |

|

|

|

x Have transparent executive compensation disclosures in our annual proxy statements |

|

|

|

x Use a thorough methodology for comparing our executive compensation to market practices |

|

|

|

x A policy that annual grants of restricted stock will utilize a vesting schedule of not less than three years |

|

|

|

x Retain an independent compensation consultant that reports solely to our compensation committee, and that does not provide our compensation committee services other than executive compensation consulting |

|

|

|

x Cap payouts on incentive awards |

|

|

|

x Use non-discretionary, pre-established, objectively determinable performance goals for our incentive awards |

|

|

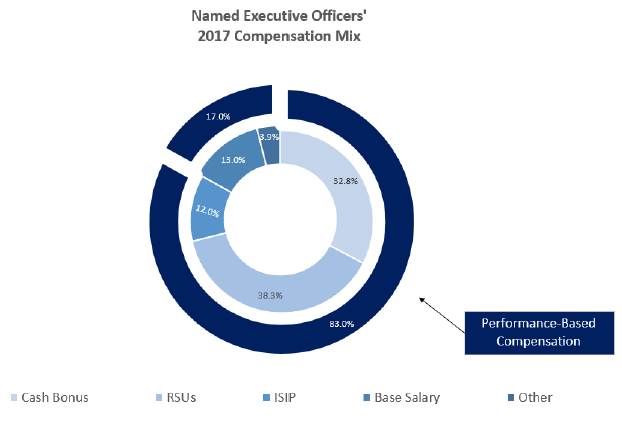

Components of Total Compensation and Pay Mix

We compensate our executive officers primarily through a mix of base salary, annual cash incentives and long-term equity-based incentives. We also provide our executive officers with the same retirement and employee benefit plans that are offered to our other employees, as well as limited other benefits, although these items are not significant components of our compensation programs. The following table provides information regarding the elements of compensation provided to our named executive officers in 2017:

|

Category of Compensation |

|

Type of Compensation |

|

Purpose of the Compensation |

|

|

|

|

|

|

|

Fixed Cash Compensation: |

|

Salary |

|

Salary provides a level of assured, regularly-paid, cash compensation that is competitive and helps attract and retain key employees. |

|

|

|

|

|

|

|

Short-term Performance-based Cash Incentives: |

|

Annual Cash Incentive Tied to Financial Metrics |

|

Cash incentives under our annual incentive plan are designed to motivate our employees to work towards achieving our key annual adjusted title revenue and adjusted pre-tax title margin goals. |

|

|

|

|

|

|

|

Long-term Equity Incentives: |

|

Performance-Based Restricted Stock Tied to Financial Metrics |

|

Performance-based restricted stock helps to tie our named executive officers’ long-term financial interests to our adjusted pre-tax title margin and to the long-term financial interests of our shareholders, as well as to retain key executives through a three-year vesting period and maintain a market competitive position for total compensation. |

|

Category of Compensation |

|

Type of Compensation |

|

Purpose of the Compensation |

|

|

|

|

|

|

|

Investment/Business Specific Incentives: |

|

Investment Success Incentive Program |

|

Our Investment Success Incentive Program was designed to help us maximize our return on investment in the FNFV companies and investments by aligning a significant portion of the executive’s long-term incentive compensation with our return related to the investments. The purpose of the program was to retain and incentivize executives to identify and execute on monetization and liquidity opportunities that will maximize returns. Following the Split-Off, the Investment Success Incentive Program was assumed by Cannae and we no longer have any obligations under this program. |

|

|

|

|

|

|

|

Benefits & Other: |

|

ESPP, 401(k) Plan, health insurance and other benefits |

|

Our named executive officers’ benefits generally mirror our company-wide employee benefit programs. For security reasons and to make travel more efficient and productive for our named executive officers, they are eligible to travel on our corporate aircraft. |

Allocation of Total Compensation for 2017

The following chart and table show the average allocation of 2017 Total Compensation reported in the Summary Compensation Table among the components of our compensation programs:

2017 Compensation Mix

|

|

|

Salary |

|

Annual |

|

Performance- |

|

FNFV Programs |

|

Benefits and |

|

Total |

|

Performance |

|

|

Raymond R. Quirk |

|

11.2 |

% |

33.5 |

% |

52.2 |

% |

0.0 |

% |

3.1 |

% |

100 |

% |

85.7 |

% |

|

Anthony J. Park |

|

15.3 |

% |

30.7 |

% |

34.1 |

% |

15.8 |

% |

4.1 |

% |

100 |

% |

80.6 |

% |

|

Michael J. Nolan |

|

15.4 |

% |

38.4 |

% |

44.0 |

% |

0.0 |

% |

2.2 |

% |

100 |

% |

82.4 |

% |

|

Brent B. Bickett |

|

7.5 |

% |

22.6 |

% |

22.0 |

% |

44.1 |

% |

3.8 |

% |

100 |

% |

88.7 |

% |

|

Roger S. Jewkes |

|

15.5 |

% |

38.6 |

% |

39.0 |

% |

0.0 |

% |

6.9 |

% |

100 |

% |

77.6 |

% |

As illustrated above, a significant portion of each named executive officer’s total compensation is based on performance-based cash and equity incentives that are tied to our financial performance, stock and equity price. Combined, performance-based forms of compensation comprised between 77.6% and 88.7% of our named executive officers’ total compensation in 2017.

Our compensation committee believes this emphasis on performance-based incentive compensation is an effective way to use compensation to help us achieve our business objectives while directly aligning our executive officers’ interests with the interests of our shareholders.

Analysis of Compensation Components

Base Salary

Our compensation committee typically reviews salary levels annually as part of our performance review process, as well as in the event of promotions or other changes in our named executive officers’ positions or responsibilities. When establishing base salary levels, our compensation committee considers the peer compensation data provided by its external independent compensation consultant, Mercer, as well as a number of qualitative factors, including each named executive officer’s experience, knowledge, skills, level of responsibility and performance. Messrs. Bickett’s and Jewkes’ 2017 base salaries were unchanged from 2016. Mr. Quirk, Mr. Nolan, and Mr. Park received increases in their base salaries in 2017 to reflect their excellent performance and to move their total compensation close to the 50th percentile of market.

Annual Performance-Based Cash Incentives

We award annual cash incentives based upon the achievement of pre-defined business and financial objectives relating to our core operations, which are specified in the first quarter of the year. Annual incentives play an important role in our approach to total compensation, as they motivate participants to achieve key fiscal year objectives by conditioning the payment of incentives on the achievement of defined, objectively determinable financial performance goals.

In the first quarter of 2017, our compensation committee approved our fiscal year business performance objectives and a target incentive opportunity for each participant, as well as the potential incentive opportunity range for maximum and threshold performance. No annual incentive payments are payable to a named executive officer if the pre-established, minimum performance levels are not met, and payments are capped at a maximum performance payout level. The financial performance results are derived from our annual financial statements (as reported in our

Annual Report on Form 10-K filed with the SEC), which are subject to an audit by our independent registered public accounting firm, Ernst & Young LLP. However, as discussed below, we use financial measures as performance targets for our named executive officers that differ from the comparable GAAP measures reported in our financial statements. The incentive award target opportunities are expressed as a percentage of the individual’s base salary. Our named executive officers’ 2017 target incentive opportunities were the same as their 2016 target incentive opportunities.

The amount of the annual incentives actually paid depends on the level of achievement of the pre-established goals as follows:

· If threshold performance is not achieved, no incentive will be paid.

· If threshold performance is achieved, the incentive payout will equal 50% of the executive’s target incentive opportunity.

· If target performance is achieved, the incentive payout will equal 100% of the executive’s target incentive opportunity.

· If maximum performance is achieved, the incentive payout will equal 200% of the executive’s target incentive opportunity.

· Between these levels, the payout is interpolated.

An important tenet of our pay for performance philosophy is to utilize our compensation programs to motivate our executives to achieve performance levels that reach beyond what is expected of us as a company. The performance targets for the FNF incentive plan are approved by our compensation committee and are based on discussions between management and our compensation committee. Target performance levels are intended to be difficult to achieve, but not unrealistic. Maximum performance levels are established to limit short-term incentive awards so as to avoid excessive compensation while encouraging executives to reach for performance beyond the target levels.

In setting 2017 performance targets under our annual incentive plans, our compensation committee considered the following factors, which are discussed in more detail below:

· the Mortgage Bankers Association’s projection that mortgage originations would decline;

· our 2017 business plan, including our underlying assumptions that refinance volumes would decline by 49%, the residential purchase market would increase by 2%, and the national commercial market would decline by 6%;

· 2017 performance targets as compared to 2016 performance targets and 2016 actual performance;

· alignment of the 2017 performance targets with the investment community’s published projections for us and our publicly-traded title company competitors; and

· the effect that reaching performance targets would have on our growth and margins.

FNF Annual Incentive Performance Measures and Results. The 2017 performance goals under the FNF incentive plan were based on adjusted title revenue and adjusted pre-tax title margin relating to our title segment. We believe that these performance measures are among the most important measures of the financial performance of our core business, and they can have a significant impact on long-term stock price and the investing community’s expectations. When combined with the strong focus on long-term shareholder return created by our equity-based incentives and our named executive officers’ significant stock ownership, these two annual performance measures provide a degree of checks and balances, requiring our named executive officers to consider both short-term and long-term performance of our businesses and investments. The annual incentive performance targets are synchronized with shareholder expectations,

desired increase in our stock price, our annual budget, our long-term financial plan, and our board of directors’ expectations. Further, both measures are measures that executives can directly affect.

In the following table, we explain how we calculate the performance measures and why we use them.

|

Performance Measure |

|

How Calculated |

|

Reason for Use |

|

|

|

|

|

|

|

Adjusted Title Revenue |

|

Adjusted title revenue is based on GAAP revenue from our title segment as reported in our annual financial statements, excluding realized gains and losses. |

|

Adjusted title revenue is an important measure of our growth, our ability to satisfy and retain our clients, gain new clients and the effectiveness of our services and solutions. Adjusted title revenue is widely followed by investors. |

|

|

|

|

|

|

|

Adjusted Pre-Tax Title Margin |

|

Adjusted pre-tax title margin is determined by dividing the earnings before income taxes and non-controlling interests from our title segment, excluding realized gains and losses, purchase accounting amortization and other unusual items, by total revenues of the title segment excluding realized gains and losses. |

|

We selected adjusted pre-tax title margin as a measure for the short-term incentives because it is a financial measure that is significantly influenced by the performance of our executives, promotes a focus on operational efficiency and cost management, aligns the executives’ short-term incentive opportunity with one of our key corporate growth objectives and is commonly used within the title industry. |

The title insurance business is directly impacted by managements’ effectiveness in executing on our business strategy, and macro-economic factors such as mortgage interest rates, credit availability, job markets, economic growth, and changing demographics. Due to the year-to-year changes in these key economic factors, we do not think comparisons of financial and business goals and performance from one year to another are meaningful indicators of the rigor of our performance goals or managements’ performance in a given year. Instead, we think our performance goals and managements’ performance relative to those goals should be assessed in light of the economic environment within which the goals were established and management operated. In setting the threshold, target and maximum goals relating to the performance measures under the FNF incentive plan, the committee considered management’s expectations for 2017 with respect to forecasted originations, interest rates and the relative mix of purchase versus refinance originations. These expectations are based on forecasts available in March 2017 provided by the Mortgage Bankers Association (MBA) and Fannie Mae, anticipated rising interest rates making housing less affordable and significantly depressing the residential and refinance markets, and recent and expected industry and company trends as reflected in our 2017 strategic financial plan. We prepare a base plan as well as upside and downside scenarios, which, taken together, form the strategic financial plan and the basis of the performance measure targets. To establish threshold and maximum goals, percentage adjustments were applied to the target goals. The pre-tax title margin threshold and maximum goals were set at 2.5% below and 2.5% above the target, respectively, and title revenue threshold and maximum goals were set at 7.5% below and 7.5% above the target, respectively. Target performance levels are intended to be difficult to achieve, but not unrealistic. Maximum performance levels are established to limit short-term incentive awards so as to avoid excessive compensation while encouraging executives to reach for performance beyond the target levels. All of the goals are subject to review and approval by our compensation committee.

Our 2017 results exceeded target thresholds due to strong performance by our executive officers and numerous factors, including a 4% increase in agency title insurance premiums driven by our active management of our agent portfolio to maximize profitability and minimize claims risk, a 3% increase in direct title insurance premiums driven by

increased purchase transactions and escrow fees, and enhancements to our underwriting processes which have resulted in lower policy year loss ratios compared to older years that, in turn, allowed us to reduce our provision for claim losses in the fourth quarter of 2017.

Set forth below are the 2017 weightings of the threshold, target and maximum performance levels, and 2017 performance results under our annual incentive plan. Dollar amounts are in millions.

|

Performance Metric |

|

Weight |

|

Threshold |

|

Target |

|

Maximum |

|

Results |

| ||||

|

Adjusted Title Revenue (Title Segment) |

|

25 |

% |

$ |

6,012.5 |

|

$ |

6,500.0 |

|

$ |

6,987.5 |

|

$ |

7,205.0 |

|

|

Adjusted Pre-Tax Title Margin (Title Segment) |

|

75 |

% |

9.5 |

% |

12.0 |

% |

14.5 |

% |

14.5 |

% | ||||

The table below shows each named executive officer’s target percentage under our annual incentive plan, the calculation of their 2017 incentive awards based on the 2017 performance multiplier from the results shown in the tables above, and the amounts earned under the annual incentive plans.

|

Name |

|

2017 Base |

|

2017 Annual |

|

2017 Annual |

|

2017 |

|

2017 Total |

| |||

|

|

|

|

|

|

|

|

|

|

|

|

| |||

|

Raymond R. Quirk |

|

$ |

1,000,000 |

|

150 |

% |

$ |

1,500,000 |

|

200 |

% |

$ |

3,000,000 |

|

|

Anthony J. Park |

|

$ |

525,000 |

|

100 |

% |

$ |

525,000 |

|

200 |

% |

$ |

1,050,000 |

|

|

Michael J. Nolan |

|

$ |

630,000 |

|

125 |

% |

$ |

787,500 |

|

200 |

% |

$ |

1,575,000 |

|

|

Roger S. Jewkes |

|

$ |

630,000 |

|

125 |

% |

$ |

787,500 |

|

200 |

% |

$ |

1,575,000 |

|

|

Brent B. Bickett |

|

$ |

550,500 |

|

150 |

% |

$ |

825,750 |

|

200 |

% |

$ |

1,651,500 |

|

Long-Term Equity Incentives

In October 2017, we granted performance-based restricted stock to each of our named executive officers.

We do not attempt to time the granting of awards to any internal or external events. Our general practice has been for our compensation committee to grant equity awards during the fourth quarter of each year following the release of our financial results for the third quarter. We also may grant awards in connection with significant new hires, promotions or changes in duties.

Our compensation committee’s determinations are not formulaic; rather, in the context of competitive market compensation data and our stated pay philosophy, our compensation committee determines the share amounts on a subjective basis in its discretion and may differ among individual executive officers in any given year. Following is a brief discussion regarding the awards made in 2017.

Performance-Based Restricted Stock. In 2017, the proportion of the FNF equity awards consisting of performance-based restricted stock remained at 100% and we did not grant stock options to our executive officers.

The restricted stock awards vest over three years, provided we achieve pre-tax title margin in our title segment of 8.5% in at least two of the five quarters beginning October 1, 2017. We considered various alternative measures but we again selected adjusted pre-tax title margin because it is one of the most important and impactful measures in evaluating the performance of our core operations, as well as the performance of our executives as it is a measure that executives can directly affect. Adjusted pre-tax title margin measures our achievements in operating efficiency, profitability and capital management. It is also a key measure used by investors and has a significant impact on long-term stock price. We increased the adjusted pre-tax margin performance metric from 8% to 8.5% for these awards

because of recent and expected industry and company trends, including a rising interest rate environment, MBA’s forecasts with respect to the mortgage originations for 2018 and the Urban Land Institute’s forecast for the commercial real estate market in 2018, with the goal of setting a target that reflects superior performance compared to our title competitors. Although we considered using a longer performance period for these awards, we determined that achievement of the criteria in at least two of the five quarters beginning October 1, 2017, which is the performance period we have historically used with respect to our performance-based equity awards, was the appropriate performance period because of the difficulty in predicting future performance of the mortgage market, particularly for a period of more than one year, because it is largely driven by interest rates and other economic forces outside of our control, and because of the seasonality inherent in the title business, with the first quarter typically much weaker than the remaining quarters due to weather conditions and holidays impacting opened order activity in November and December resulting in fewer closings in the first quarter.

Adjusted pre-tax title margin is determined by dividing the earnings before income taxes and non-controlling interests from our title segment, excluding realized gains and losses, purchase accounting amortization and other unusual items, by total revenues of the title segment excluding realized gains and losses.

With respect to all restricted stock awards, credit is provided for dividends paid on unvested shares, but payment of those dividends is subject to the same vesting requirements as the underlying shares—in other words, if the underlying shares do not vest, the dividends are forfeited.

Business/Investment Specific Incentives

The Investment Success Incentive Program. In connection with the Split-Off, Cannae assumed the Investment Success Incentive Program and we no longer have any obligations under the program.

The Investment Success Incentive Program was a performance-based cash incentive program that our compensation committee established in 2014 to help us maximize the returns on our investments in One Digital (formerly Digital Insurance) and other investments. Under the program, amounts were earned upon liquidity events that result in a positive return on our investment. For this purpose, return was determined relative to the value of our investment in One Digital as of July 1, 2014, which was $70,800,000. Upon a liquidity event, 10% of any incremental value is contributed to an incentive pool and payments are made to participants based on their allocated percentages of the pool, which are as follows: Mr. Park 2%; and Mr. Bickett 12%. Since Messrs. Quirk, Jewkes and Nolan focus on our core title business and did not focus our FNFV businesses, they did not participate in this program.

On June 6, 2017, prior to the completion of the Split-Off, FNFV completed the sale of One Digital to Achilles Acquisition LLC. As a result of the sale, FNFV indirectly received $331,301,000, of which $5,365,000 was held in escrow to cover any indemnity claims. This represents $260,501,000 in excess of the $70,800,000 base value of the investment used to measure gain for purposes of the awards. Because of the escrow holdback, our compensation committee, exercising negative discretion, determined to pay only $25,514,000 of the incentive attributable to the sale in 2017, and held back the remaining $536,000 allocated to the incentive pool pending the distribution of the escrowed funds.

Because the Investment Success Incentive Program was assumed by Cannae in connection with the Split-Off, the $536,000 remaining in the incentive pool may be paid at the discretion of Cannae’s compensation committee, and subject to the other conditions to payment contained in the incentive award agreements, such as the requirement that participants must remain employed through the payment date to be entitled to a payment.

The following table shows the return on investment relating to the sale of One Digital and the resulting payouts to the named executive officers under the Investment Success Incentive Program.

|

Name |

|

Percentage of |

|

Total Incentive |

| |

|

Brent B. Bickett |

|

12 |

% |

$ |

3,061,638 |

|

|

Anthony J. Park |

|

2 |

% |

$ |

510,273 |

|

In the sale by Ceridian of Comdata to FleetCor in 2014, the sale consideration was paid in shares of FleetCor common stock, with approximately 25% held in escrow to cover any potential indemnity claims, and any remaining escrowed funds payable to Ceridian in annual 1/3 installments over three years. As a result of the sale, we indirectly acquired (through our approximately 32% ownership interest in Ceridian) approximately 2.39 million shares of FleetCor common stock, with 25% of those shares held back in the indemnity escrow. The sale resulted in payments being made under the Investment Success Incentive Program in 2014; however, our compensation committee exercised discretion reserved under the Investment Success Incentive Program and reduced the incentives payable in 2014 by 25%, which we refer to as the Holdback Amount. In accordance with the Investment Success Incentive Program terms, our compensation committee reserved the right to decide whether the Holdback Amount (or a portion of it) would be forfeited or whether it would be paid to the participants at a future date. In November 2016, approximately 50% of the remaining escrow holdback was released from escrow and Cannae distributed approximately 50% of the Holdback Amount remaining after the November 2016 release.

The following table shows the payments made to our named executive officers in connection with the 2017 release of the Holdback Amount.

|

Name |

|

Percentage of |

|

Total |

| |

|

Brent B. Bickett |

|

10 |

% |

$ |

156,000 |

|

|

Anthony J. Park |

|

2 |

% |

$ |

31,000 |

|

Benefit Plans

We provide retirement and other benefits to our U.S. employees under a number of compensation programs. Our named executive officers generally participate in the same compensation programs as our other executives and employees. All employees in the United States, including our named executive officers, are eligible to participate in our 401(k) plan and our employee stock purchase plan, or ESPP. In addition, our named executive officers are eligible to participate in broad-based health and welfare plans. We do not offer pensions or supplemental executive retirement plans for our named executive officers.

401(k) Plan. We sponsor a defined contribution savings plan that is intended to be qualified under Section 401(a) of the Internal Revenue Code. The plan contains a cash or deferred arrangement under Section 401(k) of the Internal Revenue Code. Participating employees may contribute up to 40% of their eligible compensation, but not more than statutory limits, which were generally $18,000 in 2017. Vesting in matching contributions, if any, occurs proportionally each year over three years based on continued employment with us.

Deferred Compensation Plan. We provide our named executive officers, as well as other key employees, with the opportunity to defer receipt of their compensation under a nonqualified deferred compensation plan. None of our named executive officers elected to defer 2017 compensation into the plan. A description of the plan and information regarding our named executive officers’ interests under the plan can be found in the Nonqualified Deferred Compensation table and accompanying narrative.

Employee Stock Purchase Plan. We maintain an ESPP through which our executives and employees can purchase shares of our common stock through payroll deductions and through matching employer contributions. At the end of each calendar quarter, we make a matching contribution to the account of each participant who has been continuously employed by us or a participating subsidiary for the last four calendar quarters. For officers, including our named executive officers, matching contributions are equal to ½ of the amount contributed during the quarter that is one year earlier than the quarter in which the matching contribution was made. The matching contributions, together with the employee deferrals, are used to purchase shares of our common stock on the open market. For information regarding the matching contributions made to our named executive officers in 2017 see “—Summary Compensation Table.”

Health and Welfare Benefits. We sponsor various broad-based health and welfare benefit plans for our employees. Certain executives, including our named executive officers, are provided with additional life insurance. The taxable portion of the premiums on this additional life insurance is reflected in the “Summary Compensation Table” under the column “All Other Compensation” and related footnote.

Other Benefits. We continue to provide a few additional benefits to our executives. In general, the additional benefits provided are intended to help our named executive officers be more productive and efficient and to protect us and our executives from certain business risks and potential threats. For example, in 2017, certain of our named executive officers received personal use of the corporate aircraft. Our compensation committee regularly reviews the additional benefits provided to our executive officers and believes they are minimal. Further detail regarding other benefits in 2017 can be found in the “Summary Compensation Table” under the column “All Other Compensation” and related footnote.

Employment Agreements and Post-Termination Compensation and Benefits

We have entered into employment agreements with each of our named executive officers. These agreements provide us and the executives with certain rights and obligations following a termination of employment, and in some instances, following a change in control. We believe these agreements are necessary to protect our legitimate business interests, as well as to protect the executives in the event of certain termination events. For a discussion of the material terms of the agreements, see the narrative following “—Grants of Plan-Based Awards” and “—Potential Payments Upon Termination or Change in Control,” below.

Role of Compensation Committee, Compensation Consultant and Executive Officers